Historically, stock valuations have been an important predictive factor of future returns. A standard practice is to measure value by comparing stock prices to fundamental measures such as trailing earnings, projected earnings, dividends, and book value. I am increasingly questioning the usefulness of these measures however. While an enormous body of research has shown that stocks that are relatively low priced compared to their earnings or book value have historically tended to out-perform, the so-called value effect has now suffered an incredibly long period of failure.

The standard practice in investing is to classify stocks as either value (low price compared to earnings, dividends, or book value) or growth (high price compared to these measures). There are many indexes and index funds that track the performance of stocks sorted by growth and value.

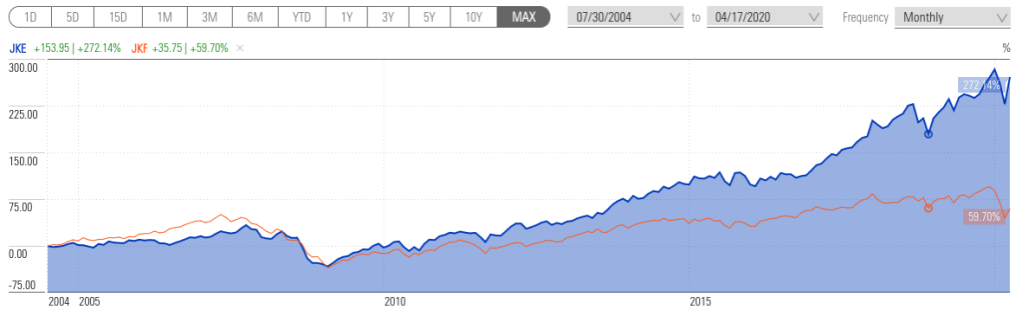

The iShares Large Cap Growth ETF (JKE) has absolutely crushed the iShares Large Cap Value ETF (JKF) since inception and this relative performance is representative of the major indexes. In fact, growth has out-performed value over every recent time horizon. For the year to date, JKE is down 1% but JKF is down almost 19%.

I have written a couple of blogs (see here and here) about the apparent dwindling of the value effect, and the asymmetry between value and growth in the current decline highlights the issue. Value under-performed in the long bull market from 2009 through early 2020 and has also under-performed in the recent market decline due to COVID-19.

I am starting to think that markets have evolved in ways that mean that fundamental measures of value may not matter anymore and there are a number of obvious drivers. First, the massive shift towards passive investing and index funds reduces the significance of value. Stocks that have increased in price more quickly than peers are an ever-larger component of the indexes (because most indexes are market cap weighted), which means that index investors are effectively growth investors. Second, many companies are reinvesting a higher percentage of profits in new growth opportunities rather than declaring operating earnings and investors have been trained to be okay with this. Amazon is the classic example. As such, reported earnings have less impact of how investors select stocks. Third, I think that investors increasingly view stocks as a store of value, much as they might think of bitcoin, gold, or dollars. Shares are symbolic of value rather than being considered as physical ownership stakes in companies. As such, measures of fundamental value are less effective as predictors of return.

The enormous literature on the out-performance of value stocks must be set against the obvious truth that markets evolve. When investors expected to receive dividends as a substantial component of returns, earnings were a matter of considerable interest. Dividends are paid out of earnings. When investors no longer receive a share of earnings in the form of dividends, earnings are essentially an abstract bookkeeping concept. A much smaller fraction of public companies pay dividends than in the past and the tech sector, the massive out-performer of the last couple of decades, has very few dividend payers.

The data showing the predictive value of earnings for future returns largely come from periods of history that were very different in terms of the types of economically dominant sectors and companies. The world changes. Many of the greatly admired companies that comprised the Nifty Fifty, a group of massive firms from the 1960’s and 1970’s, are unfamiliar to most investors today. Back then, these companies were household names for investors and everyone wanted to own them. Looking at these companies as a measure of how the world changes may also serve to remind us of what can happen when investors disregard fundamental value. The Nifty Fifty are also remembered because they were the hot growth stocks of their time, and investors ignored fundamentals in choosing to buy these stocks. The Nifty Fifty ultimately crashed spectacularly. Even so, the world is a very different place than it was in the decades when the efficacy of the value effect was established. It is naive to assume otherwise.

It is said that the most dangerous phrase in investing is “its different this time” and many disastrous investing strategies can be attributed to the crowd ignoring the lessons of the past. The lessons of the past must be set against the acknowledgement that markets can and do evolve. While value investing may stage a comeback, data is accumulating to suggest that perhaps the value effect is dead, or at least greatly reduced.