Research Affiliates, a large money manager and research firm, has recently reaffirmed it’s faith in value investing, the discipline of investing more heavily in stocks which appear cheap relative to their earnings or book value.

Back in April of 2019, I wrote a blog post that explored the under-performance of value over the last fifteen years. My guess back then, as it remains, is that value will eventually experience a recovery, just based on the fact that out-of-favor investing styles tend to come back into fashion at some point. The question is how long it will take for a turnaround to occur.

The substantial shift in the ways that corporations manage their finances makes me wonder whether the past is all that great a guide in this instance. Specifically, value stocks tend to be those that have lower-growth businesses. Value investors expect to pay a relatively low price per dollar of current earnings because of limited growth potential. Part of the historical appeal of such stocks is that they paid higher-than-average dividends. Today, investors seem to favor higher growth and there are relatively few investors who care about dividends.

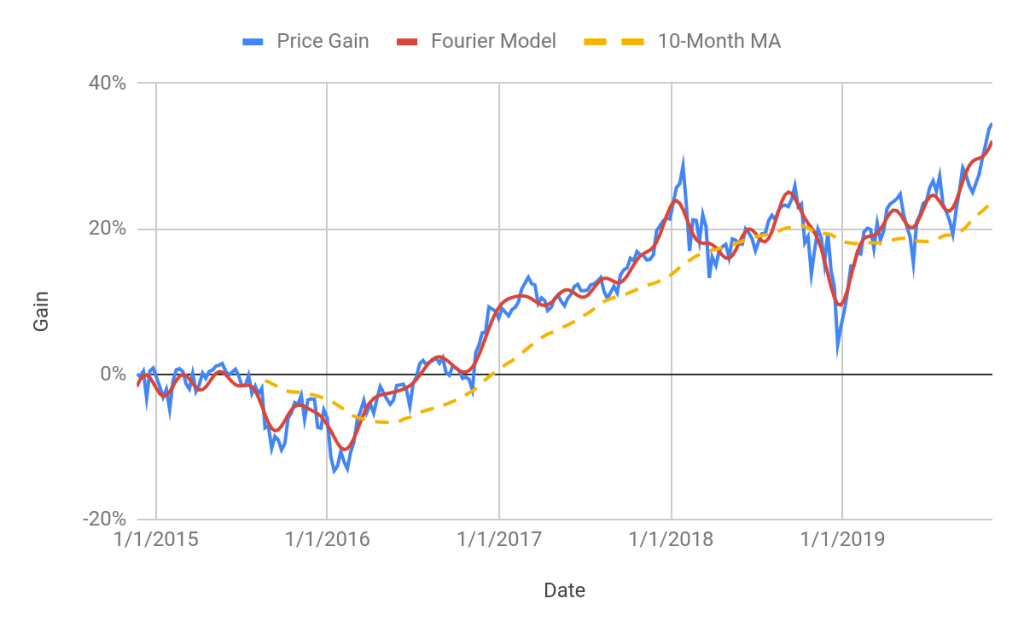

Looking at the past five years of performance for the iShares S&P500 Value ETF (IVE) and the iShares S&P500 Growth ETF (IVW) is quite interesting (see the two charts below). These charts show cumulative price return (no dividends) since the start of the five year period (Price Gain), an econometric smoothing model (Fourier model), and the 10-month moving average (10-Month MA).

The five-year total return for IVE is 8.64% per year, as compared to 12.46% per year for IVW. The purpose of looking at these charts is to see whether there is any evidence that the trends are changing, such that value might start to catch up with growth in the near future. Both IVE (value) and IVW (growth) show substantial trends over the period and both had a big drop at the end of 2018 and a robust recovery in 2019. Note, however, that there are much larger short-term swings in IVE relative to its trend, as compared to IVW. In the parlance of econometrics, a great deal more of the variance in IVE is high-frequency (short-term fluctuation).

Over the past three years, IVW has slightly lower volatility than IVE (annualized volatility of 12.15% for IVW vs. 13.13% for IVE), but the differences in total volatility don’t tell the whole story. The volatility is associated with difference time scales. IVW’s volatility is more associated with its long-term trend. The short-term volatility in IVE is so great that, at the end of 2018, the price of IVE dropped almost to its value at the start of the five year period. IVW took a big hit, too, but the loss was far smaller as compared to gains earlier in the five-year period.

Volatility is an expression of the market’s uncertainty as to the future prospects for a stock or asset class. Low-frequency variability (fairly slow changes around the trends) suggest an evolving view. High-frequency variability suggests that there is a lot of near-term uncertainty, such that the consensus outlook is very unstable.

Econometric models (including trend analysis, moving averages, Fourier analysis) are conceptually useful to see how the market’s consensus estimates of fair price change through time and they are not a solver bullet by any means. Looking at these value and growth index ETFs suggests considerably more fear, uncertainty, and doubt in value than in growth. Certainly, one might suggest that the continued run for growth is an expression of complacency and I think there is some truth to that. My overall conclusion, however, is that value shows no signs (as yet) of a meaningful recovery relative to growth.