The foundation of fundamental analysis is determining whether companies, sectors, and markets are expensive or cheap relative to measures of their inherent value. The most commonly-cited measure of value for stocks is the price-to-earnings (P/E) ratio. We might look at the most-recent year’s earnings, the standard for P/E, or average earnings over a longer period of time (ten years in Schiller’s P/E 10 ratio). Historically, it has been more profitable to invest when P/E is lower than average and vice versa. This is not surprising. There is, however, a logical fallacy in concluding that P/E, in whatever form, can be used to make a go / no-go decision on investing in an specific environment.

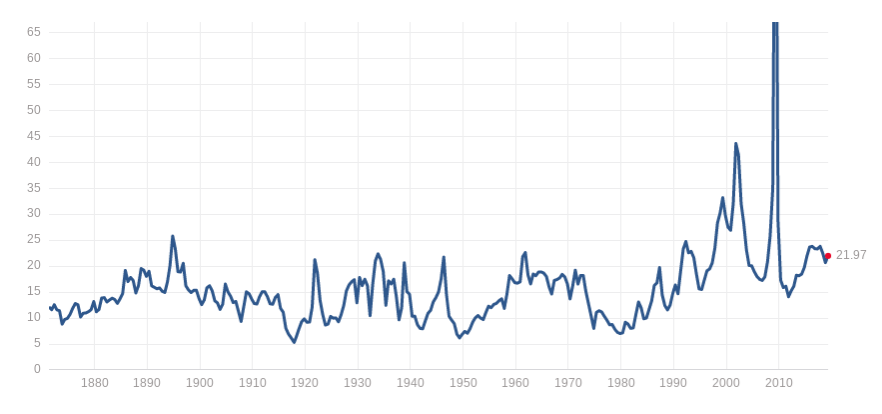

It is straightforward to compare peaks and valleys in P/E to periods of subsequent higher or lower returns. P/E 10 is more widely used than the traditional P/E ratio because P/E 10 has historically been a better predictor of returns in subsequent periods.

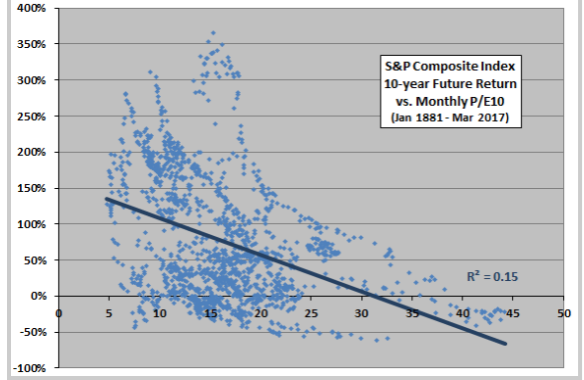

A common way to look at the relationship between P/E 10 and and subsequent returns is by looking at all possible 10-year return periods and the P/E 10 that they started from. An example is below.

Historically, the maximum 10 year returns on the S&P 500 starting from P/E 10 greater than 20 have been much lower than those for for periods starting with lower P/E 10. In periods starting with P/E 10 greater than about 37, the subsequent 10-year returns have all been negative.

The charts and references above seem to provide a compelling argument that it is unwise to be heavily invested in stock when the P/E 10 is greater than about 20. On the other hand, most of the current stock rally, starting in 2009, has occurred with P/E 10 values greater than 20. Furthermore, since the early 1990’s, the P/E 10 has spent very little time below 20.

While P/E 10 and traditional P/E are useful measures, the problem is that P/E measures have to be considered against a backdrop of a range of other variables. First, the ways that corporations manage their finances has changed over recent decades. Investors are more willing to see low earnings as suggesting that a company is investing in growth (Amazon is a famous example). Companies are catering to increasing investor demands for growth and, as a result, not worrying much about generating high-quality earnings streams. This effect increases P/E values. Second, P/E values have to be considered relative to other investment alternatives. One comparison is to look at P/E values in different interest rate environments. When bond yields are low (as they have been for years), it is entirely rational for investors to be willing to invest in stocks at higher P/E ratios–and that is exactly what we see. A third reason why looking at P/E in isolation may not be useful is simply that the markets and the global economy change over time. Even the concepts of reported earnings evolves. Furthermore, as wealth becomes more concentrated, the baseline long-term P/E should increase because there is more wealth looking for profitable opportunities.

While I consider P/E 10 to be a good measure to keep an eye on, I don’t think that it is terribly useful as the basis for investment decisions in isolation. P/E 10 is undeniably well-above above its long-term average. Historically, high P/E presages lower future returns, and that makes sense from an economic standpoint as well as being clearly evident in historical market data. The question for investors is whether there are alternatives to equities that might provide reasonable returns at comparable risk levels–and this is where U.S. stocks remain attractive. Even if the future returns on U.S. stocks are modest by historical standards, they are still quite likely to be the best current choice among the riskier investment classes.