Carrying debt can have costs far beyond the interest paid, something that few people fully appreciate. Debt repayment has substantial opportunity costs, which means that there are decisions that are unavailable because you are repaying debts. A substantial component of these opportunity costs relates to tax benefits.

Lost tax benefits

The single most important opportunity cost of debt is that repayment may consume money that would otherwise be saved in accounts that reduce taxable income. Tax-deferred savings accounts for retirement (401(k)s and IRAs), for education (529 plans) and healthcare (HSAs) are enormously valuable. Money spent on debt repayment is after-tax, while money contributed to tax-deferred savings accounts such as 401(k)s and IRAs is pre-tax. HSA contributions are pre-tax and withdrawals for health expenses as entirely pre-tax, too. 529 plan contributions typically have state tax benefits on contributions, but withdrawals for educational expense are entirely tax free. Pre-tax savings reduce taxable income and may even be enough to push you into a lower tax bracket. When debt payments offset the ability to reap these tax benefits, this is an additional cost of debt.

Missing out on employer 401(k) matching

Many employers offer their employees matching money in a 401(k). The specifics of these programs vary, but the employer typically contributes to a 401(k) in an amount that grows with employee contributions. A dollar-for-dollar match means that the employer contributes a dollar for each dollar the employee saves, up to some amount. If you don’t contribute to your plan, you don’t get the matching money. American workers are missing out of tens of billions of dollars in retirement savings by not contributing enough to get the full employer match.

Losing years of investment growth

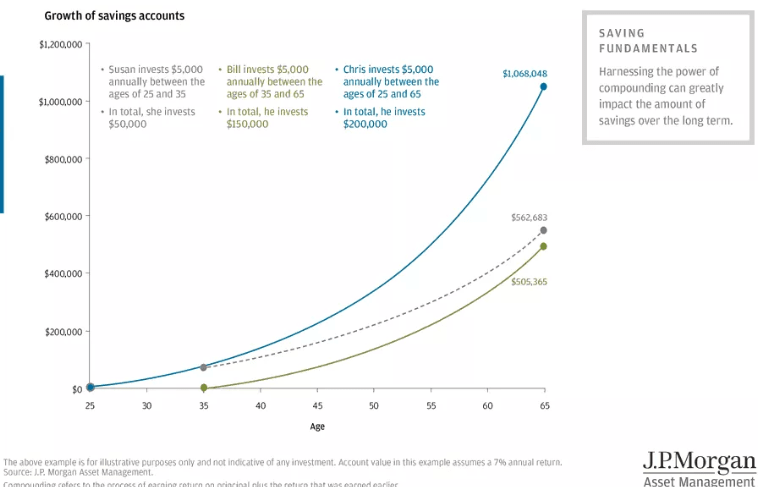

Another form of opportunity cost of debt relates to the number of years that you have available for building wealth. If are paying off debts and delay investing, the amount that you will have to invest to reach a goal gets larger. The following chart shows a famous example. One person saves $5,000 per year between age 25 and 35, and then just leaves that amount invested until retirement at age 65. The other person starts investing $5,000 per year at age 35 and continues to invest this amount until age 65. The first person contributed a total $50,000 and the second person contributed a total of $150,000. If these investors earn 7% per year on their accounts, the person who saved $50,000 early will have more at retirement than the person who saves $150,000 starting later.

Labor opportunities

Someone with high debt payments is less likely to be able to pursue new career opportunities. The most common example is of people who have home mortgages and have little or no equity. If they must sell their homes in order to move for a new job, they will incur costs. There will be realtors fees and, more significantly, they may be required to pay the difference between the mortgage balance and the sale price of the home. The need to come up with this money is a dis-incentive to relocate.

More generally, taking a new job often requires some capital to cover a temporary interruption in income and to pay for one-off costs such as a security deposit on an apartment. Debt payments may preclude the ability to cover these costs.

Finally, there are many types of work that pay relatively low wages but that have substantial potential. Startups typically don’t have pay much in salary, but they can be very attractive places to work. Someone with substantial debt payments may be unable to leave a job with more security and higher current pay to join a startup.

Discussion

The total costs of debt are higher than most people realize. Someone who incurs debt early in life will have less money for saving in tax-advantaged accounts such as 401(k)s, IRAs, and Health Savings Accounts. In many cases, people are not saving enough to get the full matching money offered by employers. In addition to lost tax benefits and employer matching money, delayed savings reduces the opportunity to build wealth due to missed years invested. Simply put, if you start saving later in life, it is very hard to catch up. Finally, debt repayment may preclude attractive career paths that result in lower current income.

As I note in a recent post, American households are taking on more debt relative to income than in previous generations. While this supports higher current consumption, the long-term impacts on financial health and opportunity are higher than many people realize.