I have followed news of the surge in the number of people quitting their jobs, aka The Great Resignation, with considerable interest. The number of people quitting their jobs reached 4.5 million in November, an all-time record. The labor force participation rate had its largest 12-month drop on record for 2020 and remains well below pre-pandemic levels. Unemployment is very low and the number of job openings is high. What is going on?

There are a number of drivers of The Great Resignation that have aligned to create a significant shift in the labor markets:

- Government aid related to COVID

- Strong investment gains in recent years

- The hiatus in college debt repayment

- Parents staying home to look after school-aged children

- Older workers leaving the workforce

- People taking early retirement

- Younger people job hopping

- Shift in perception of acceptable work-life balance

Perhaps the most obvious cause of people staying out of work is that they can afford not to be employed, thanks to the range of government assistance during COVID. Government help comes in various forms, including stimulus checks, extended unemployment benefits, the eviction moratorium, and the pause in student loan repayments. Booming housing and stock markets have also increased household wealth in recent years. Americans added an estimated $4 Trillion to their savings (including investment gains) during COVID. When cash reserves from government payments run out, student loans return to normal payment status, and people spend investment gains or the market turns, there will be an influx of people to the workforce.

I distinguish between #5 and #6 on the basis of research by Boston College Center for Retirement Research that concluded that many of the older workers who have quit their jobs may be considering a return to work in the future (#3). COVID resulted in a marked increase in people 55+ leaving their jobs, but there was not an equivalent jump in the number of people self-identifying as retired or claiming Social Security. COVID also appears to have motivated 3 million Americans to retire early. The substantial gains in the stock market and in house values have made early retirement more possible and attractive for many older workers. It is possible, however, that some fraction of these people will re-enter the workforce when they see health risks as low enough, when savings drop sufficiently, or wages rise enough to entice them.

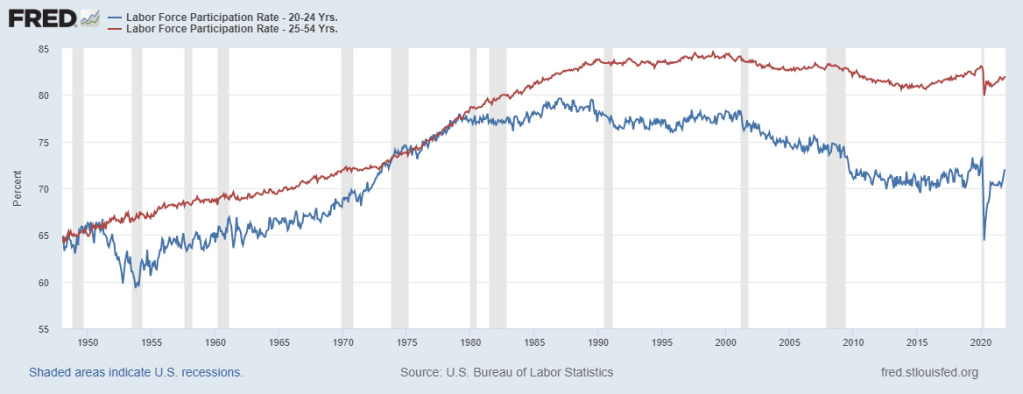

While Millennials and Gen Z’ers tend to hold jobs for shorter periods of time than older people, it is not clear that younger workers are leaving the workforce in The Great Resignation–they are just job hopping. The labor force participation rate for people aged 25-54 is currently 81.9% and is rebounding rapidly from the COVID-driven decline. The labor force participation rate for people aged 20-24 has been declining for years, largely due to increased time in higher education, but has bounced back sharply from COVID and is approaching the pre-pandemic level.

A great deal has been written relating The Great Resignation to people questioning the prevailing norms of work-life balance (also see this article). Significant changes in societal norms often correspond to periods of crisis, and COVID may be just such a disruptive event. A relevant example is how World War II resulted in a substantial shift in perceptions about the types of work that women could (and should) do. COVID may have long-term impacts on the ways that people think about how employment works. It is clearly harder for employers to insist that employees commute to a centralized office in order to be effective after this extended period during which many companies have performed very well with a fully-remote workforce.

The ultimate changes to labor markets related to, or inspired by, The Great Resignation will be years in the making. Right now, unionization and strikes are both seeing upticks as workers capitalize on the tight labor market. The influence of labor unions has been waning for decades and it is far too soon to tell whether the current shift will have a long-term impact. As the chart above shows, the labor force participation rate for people aged 25-54 (a group the government calls prime age workers) has declined over the past 20 years. In January of 1999, the primage age labor participation rate 84.6%. In January 2020, right before COVID tanked employment, this value was 83%. Today, 2 years later, the prime age labor participation rate is 81.9%. It is unclear how the last couple of years’ COVID-related events will impact the long-term variability in the percentage of so-called ‘prime age’ people with jobs. The Fed’s policy of holding down interest rates and asset purchases have boosted stock markets and the prices of residential real estate. This, in turn, allows people to retire early, to support a stay-at-home parent, or to be able to quit a job. Rising interest rates and Fed tapering of asset purchases should slow the rampant increases in house prices, but the impacts on equity markets are harder to predict. Theoretically, higher interest rates should limit equity markets, but equities may be a refuge of choice during this period of inflation. People make different consumption decisions when they feel richer (the wealth effect) and many U.S. households are considerably wealthier today than a couple of years ago.

The Great Resignation is a result of an unusual confluence of events that may have limited long-term effects on the labor market. There is some potential for persistent shifts that will benefit workers, however. Increased bargaining power for employees may be a secular shift, after decades of declining influence. Remote work is likely to stick around, now that employees and employers have seen concrete evidence of how well it works. I will not be surprised if we are see a long-term increase in early retirement and career downshifting, partly initiated by COVID but reinforced by workers’ shifting perceptions of the relative attractiveness of higher consumption vs. more time and less stress.