A number of years ago, while being interviewed, University of Chicago professor Harold Pollack asserted that everything you need to know about personal finance can fit on an index card. The idea got massive media coverage and went viral because so many people think that personal finance is complicated. The interviewer, Helaine Olen, and Dr. Pollack subsequently collaborated on a 245-page book titled The Index Card: Why Personal Finance Doesn’t Have to Be Complicated. At this point, the reader is probably asking themselves why you need to read a 245-page book if everything you need to know will fit on a single 3×5 card. We can either conclude that (1) you really don’t need more than a 3×5 card but the authors were offered a book deal to capitalize on their media buzz, or (2) personal finance does require more knowledge.

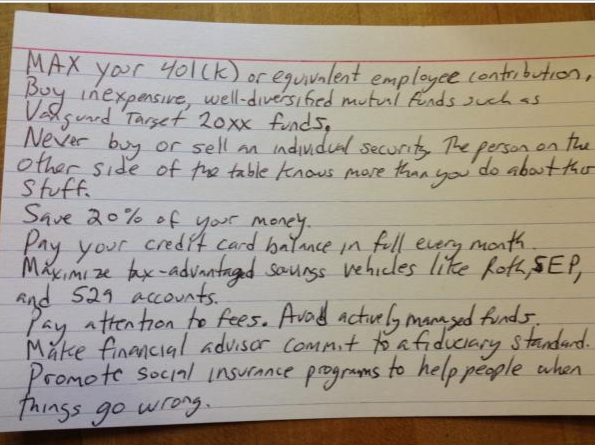

Here is Pollack’s original index card of rules:

As someone who works in finance and is interested in financial literacy, I have thought quite a bit about the challenges that people face in trying to make good financial decisions. For the vast majority of individual investors, I would agree that following all of the rules on this card would improve most individuals’ financial situations, but that does not mean that these directions are all you need to know.

The challenge of real life financial planning is in dealing with the ‘what if’ scenarios and the specifics of how things evolve. If you save 20% of your income, this is definitely better than saving less than 20% and it’s a good benchmark to shoot for (see discussions of the 50/30/20 budget), but choosing a savings rate is not trivial. You may be trying the balance the benefits of buying a home vs. reaching the 20% savings target. Is saving 20% your target if you didn’t start to save for retirement until you were 40? What if the 401(k) plan offered by your employer has a really high expense ratio? The list of real-life challenges goes on and on and this is why people will need a lot more knowledge than will fit on that index card.

People want to use money to accomplish certain things and they need to know if they are on the right track to reach these goals. Here are some of the big goal-oriented questions that people grapple with:

- Is it financially feasible for me (or my child) to attend a private college?

- Is it financially viable for me (or my child) to get a degree (BA/BS or graduate degree) in my (their) chosen field?

- Can I afford to be a stay-at-home parent?

- If I save 15% a year towards retirement, at what age can I afford to retire?

- How much can / should I spend on a home?

- Is it worth it for me to hire an investment advisor?

- If I got laid off tomorrow, could I afford to retire?

- How much do I need in savings before I can stop saving, whether or not I stop working?

- If my employer offers me a lump-sum payment to cash out of my pension, what are the tradeoffs?

- Should I pay extra on my mortgage each month / pay off my mortgage early?

- How much can I afford to contribute to my child’s college education without jeopardizing my retirement?

These are hard questions and there are many others just like these. To come up with answers, you typically require some careful estimates of a range of variables. I am not suggesting that people throw up their hands and hire an advisor to do all of this, but I do think it’s important to understand what’s involved.

Let’s also make a list of a few of the important tasks that aren’t on the index card.

- Maintain a list of your major financial goals (when you want to reach each goal and how much it will cost)

Unless you specifically lay out financial goals, including when and how much you will need, it is not really possible to create a financial plan.

- Maintain a personal balance sheet (a list of all assets and all debts)

The personal balance sheet is a summary of where you are financially. The personal balance sheet also shows the rate at which you are making progress or losing ground in terms of paying off debts and building wealth.

- Check in on your progress towards goals regularly (at least once per year)

Checking in on how things are progressing is crucial in either reinforcing what you are doing or realizing something needs to change. Without regular checkups, it’s hard to know how you are doing.

- Estimate your life expectancy using an online calculator

One of the most important factors in retirement planning is having a general sense of your life expectancy. There are a number of good online calculators available. Life expectancy helps you know when you can retire, how much you need to accumulate, and when to claim Social Security.

These are examples of some of the important things that people need to understand, think about, and act on that are not on the index card. This is not a critique of Dr. Pollack’s card, but rather a view of the range of things that people need to include as part of financial planning.

For most people, the question will be whether they are willing to take on the responsibility of handling these tasks or whether they should hire a financial planner or advisor. If you are so inclined, taking on these tasks yourself will be empowering and nobody will ever care as much about whether you reach your goals as you do. On the other hand, many people hate spending time on goal setting and financial planning. It is better to pay someone than not to plan.

Dr. Pollack’s notecard has a series of rules that will be very helpful for most people. Even so, financial planning includes many decisions that require more consideration and knowledge. Web-based financial tracking, planning and investing apps can help but people need to be engaged and proactive or have someone who can help in formulating financial plans and making key decisions.