Elizabeth Warren and Bernie Sanders have proposed massive college debt forgiveness programs. I am not in favor of these proposals, largely because of the general unfairness of having taxpayers subsidize people who have attended expensive private colleges or made other costly personal education choices. This is unfair to families that scrimped and saved or made less-expensive choices, as well as to people who didn’t attend college at all. We know that college graduates tend to have much higher incomes than non-graduates. The median high school graduate makes about $718 per week, as compared with $1,189 for the median worker with just a bachelor’s degree and $1,451 for the median worker with an advanced degree. About one third of American adults have a bachelor’s degree or higher. It is unconscionable to propose that the two thirds of people making a median wage of $718 per week should pay off the education debts of people earning 55% to 100% higher incomes (bachelor’s and advanced degrees, respectively) as a result of their educations. It is intellectual elitism at its worst to propose that a working class household should pay the educational debts of someone who attended an expensive private college but who chose to enter a field with relatively low income (and thereby qualifies for maximum debt forgiveness).

The total college debt burden in the U.S. is about $1.5 Trillion. Even if this amount could be funded by taxing the very wealthy, I believe that there is a much more constructive and fair use of this money. If we, as a nation, are going to engage in a massive large-scale one-time giveaway of money, I have an alternative that is much more sensible. I propose that we open and fund an individual retirement account (IRA) for every single American at or below the median household income (currently $62,000), a concept that we might call IRAs for All.

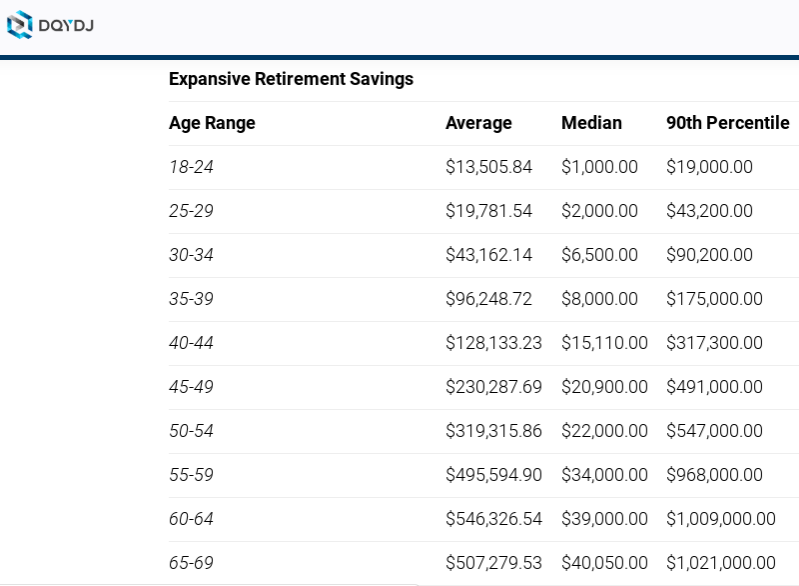

Let’s do some basic calculations. With about 330 million people in the U.S. and looking at an alternative use of the $1.5T, we could fund an IRA with $4,500 for every single person. If we limit the provision to median or lower household incomes, this jumps to $9,000 per person–including children. This would be a huge benefit for the median household in America. When we sum up all dedicated retirement savings (IRAs, 401(k)s, and similar accounts) and all liquid financial assets (stocks, bonds, mutual funds, etc.), total median savings are low. The median household headed by someone in the age range from 40 to 44 has total savings of $15,110 (see below). The average number of people in a U.S. household is 2.5. At $9,000 per person, the median household and below would gain $22,500 in retirement savings (assuming that the median income household tends to also match the average number of people).

Source: https://dqydj.com/retirement-savings-by-age-united-states/

Let’s think through the implications and creating the IRA for All rather than paying off college debt. First, while college debt is a problem, the retirement savings crisis that we face in the United States is far more serious. For the median household with the head of household between ages 45 and 54 to have only $21,000 to $22,000 in total liquid assets demonstrates that we have a massive systemic problem. Those who note that most of today’s seniors are doing fine are entirely missing the point. Today’s seniors look nothing like those of the future. Current retirees were vastly more likely to have traditional pension plans, for example. The number of Fortune 500 companies offering traditional pensions declined from 251 in 1998 to 34 in 2013. In addition, changes to Social Security laws in 1983 mean that people reaching age 65 in 2025 or later will receive almost 20% less in benefits that current retirees. And, of course, people are living longer than in previous generations, necessitating more in savings to support themselves during retirement. See this paper for a discussion of how future retirees are facing a very different situation than previous generations. Working until later ages may be a partial solution, but cannot solve the problem, especially for lower-skill workers. While there is no absolute benchmark, the consensus among economists is that the majority of future retirees will be reaching retirement age with far too little in assets to sustain anything close to their pre-retirement standards of living.

There is no question that college debt forgiveness plans provide disproportionate benefits to higher earners, while funding IRAs for lower-income households provides benefits to everyone, regardless of whether they went to college or not. Brookings calculates that the 20% of households with the highest earnings would reap 27% of the financial benefits from Warren’s proposal. The IRA for All concept provides all of its benefits to the median- and lower-income households. As one would expect, lower income households have much less in retirement savings, so the relative benefit of these proposed government-funded IRAs is much more significant for below-median-income households.

College debt forgiveness creates moral hazard by rewarding people who make the wrong choices and penalizing people who make better choices (I am asserting that someone who borrows money that they cannot repay has made a bad choice). In addition, college debt forgiveness sets a dangerous precedent that the government (e.g. taxpayers) should pay the debts resulting from individuals’ poor choices. Once we forgive college debt, why not pay off credit card debt? The IRA for All concept suffers from neither of these problems.

College debt forgiveness provides funds to many people to whom the debt is not an undue burden, as well as to those who make worse choices (attending more expensive schools, saving less, not taking work study, not starting at community college, etc.). There are people who are substantially burdened in paying off their college debts, but are they more deserving of taxpayer money than a non-college-educated working family that has accumulated little or no retirement savings? I think not. Some of the arguments favoring debt forgiveness focus on the economic stimulus of having the newly unburdened college graduates able to spend more money, but this is surely true if we funds IRAs for lower-income households, too. If we, as a nation, are considering a $1.5 Trillion one-time payment to improve the lot of American families, the IRA for All is much fairer and more equitable than college debt forgiveness.