I wrote posts in January and March sharing my thoughts on market conditions so far in 2025. Early in the year, markets shifted rapidly from general concern to a state of considerable fear, with a corresponding sell-off in U.S. stocks, as the Trump administration has worked through its tariff policies. As the rhetoric has settled down, markets have bounced back, although the question of long-term tariffs remains unsettled. In addition, the increasing tensions between Iran and Israel are a destabilizing influence on markets.

Market Volatility

As I noted in my March post, it is important to think about recent volatility in the context of longer periods. While market volatility skyrocketed in the wake of the “reciprocal tariff” announcement(s), current levels of volatility are close to longer-term averages. Market volatility, as measured by VIX (an index that tracks current volatility of the S&P 500), is running at 20.5% (annualized, as of June 20th). Note: VIX is quoted as a number without the percentage sign, but it represents the annualized percentage of standard deviation in return, otherwise known as volatility. A VIX of 30 corresponds to annualized volatility of 30%, for example. VIX reached a maximum of about 53 during the worst tariff-driven turmoil in April (volatility of 53%). The average volatility for the S&P 500 over the past 3-, 5-, and 10-years years is about 16.6%, 16.2%, and 15.5% (respectively). Volatility skyrocketed in April, but has since fallen to a level that is not much higher than the long-term average. Options on the S&P 500 expiring in January of 2026 indicate that the expected volatility (what is called implied volatility) between now and early 2026 is 19.3%. This is slightly lower than current volatility, but still above the long-term averages. Note: the VIX index is the implied volatility of options that expire over the next 30 days. In summary, volatility fallen rapidly as tariff-related panic has abated. The outlook for volatility is to remain modestly elevated into the start of 2026.

Inflation and Interest Rates

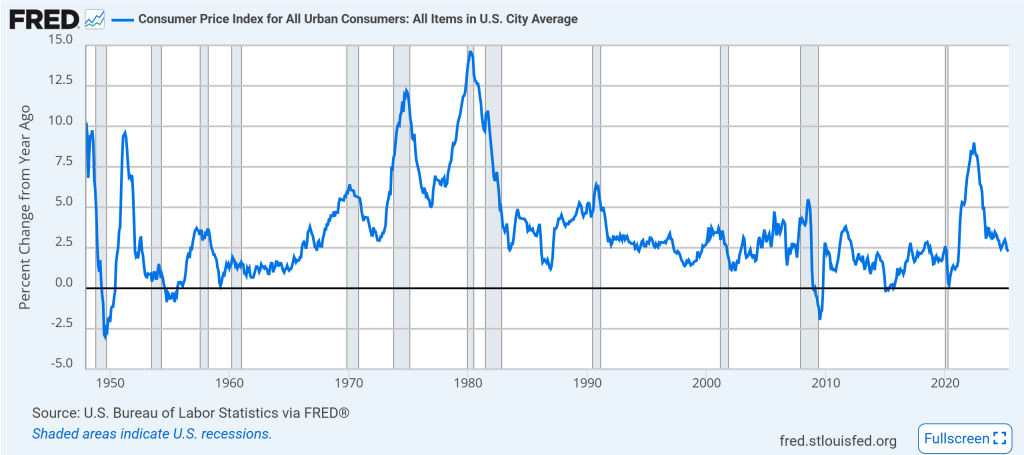

U.S. inflation has fallen dramatically since mid-2022, when the year-on-year change in CPI reached 9% in June of that year. Currently, the 12-month change in CPI is about 2.4%. This level is on the high end of the range from 2010 to the start of 2020, but is fairly modest relative to the long-term average.

The outlook for fixed income (bonds) is challenging. While the returns on intermediate Treasury bonds has been quite strong so far in 2025, with the iShares 7-10 Year Treasury Bond ETF (IEF) having a YTD total return of 3.96%, the longer-term returns are sobering. The trailing 10-year total return on IEF is 0.97%. With the trailing 10-year average U.S. inflation rate of 2.9% (through 2024), investors in IEF have lost money relative to inflation over the last decade.

The negative real return (return net of inflation) for intermediate Treasury funds is not an anomaly. The Vanguard Total Bond Market ETF (BND) and the iShares Core U.S. Aggregate Bond ETF (AGG) have trailing 10-year return of 1.6% per year, and 1.59% per year (respectively), for example.

With the U.S. government on a trajectory that is expected to result in massive growth in the deficit, bonds look less attractive in the mid- to long-term. In the near-term (the next 12 months), the Fed expects to cut interest rates, which would tend to increase the returns to bond investors. The probability of rate cuts will be sensitive to ongoing inflation, with uncertain impacts of tariffs. In general, tariffs increase prices (increase inflation), although U.S. consumers have yet to really feel this effect.

Summary Market Outlook

With the recovery from the market swoon of early April, both the S&P 500 and NASDAQ 100 indexes are very close to their all-time highs. The trailing 12-month inflation rate continues to fall, although it is still somewhat elevated relative to the baseline level prior to the jump in inflation that started in 2020. The overall economic outlook for the U.S. appears surprisingly robust in the face of uncertainties in policy and geopolitical tensions. To quote the most recent Federal Open Market Committee (FOMC) statement, “recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.”

With the U.S. government showing a distinct lack of economic discipline, along with the related international sell-off in U.S. Treasury bonds, it is hard to feel much enthusiasm for this asset class. There are money market funds and high-yield savings accounts that are yielding over 4%, while 20- and 30-year Treasury bonds are yielding around 4.9%. Any rate cuts will have a higher benefit for investors in longer-term bonds, but of course this rate sensitivity cuts both ways. As in my previous market outlooks in 2025, shorter-duration bonds look more attractive. Longer-term bonds don’t seem to provide sufficient additional yield to justify the elevated sensitivity to inflation and other interest rate drivers.

Overall, I remain in the TINA (There Is No Alternative) camp with regard to U.S. equities. U.S. companies continue to perform amazingly well in spite of tariff uncertainty. We are seeing amazing innovation in AI applications, and the consensus outlook is that AI should boost productivity. That said, there is certainly a lot of hype around AI as well. Consistent with my market outlooks from earlier this year, I conclude that we are in a ‘stay the course’ situation with U.S. equities.